Fintech

Economy Rebounds on Import Drop and Consumer Strength | PYMNTS.com

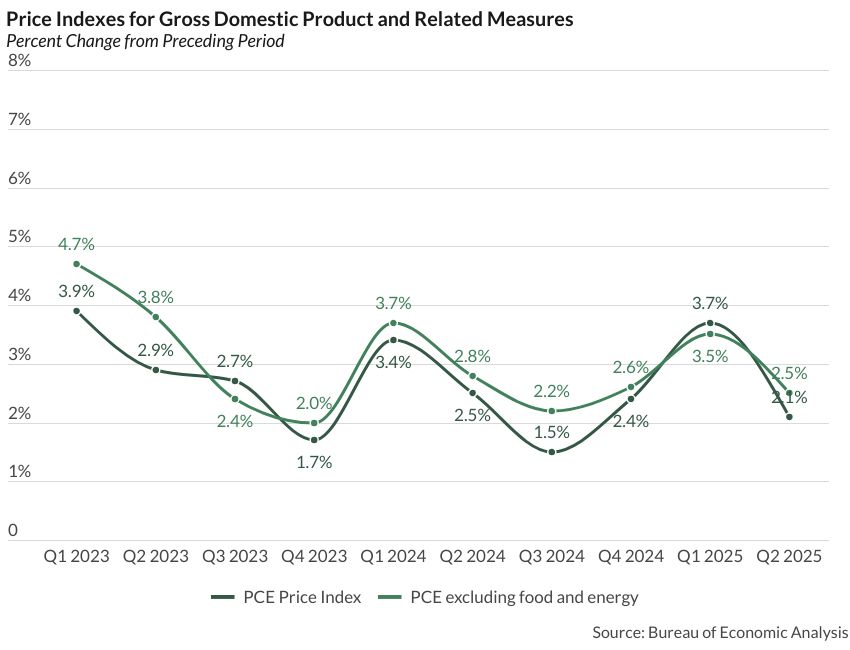

A drop in imports and a pickup in consumer spending led real gross domestic product (GDP) to return to growth in the second quarter, according to the Bureau of Economic Analysis (BEA) advance estimate for the second quarter released Wednesday (July 30).

Data analytics/artificial intelligence (AI) firm Databricks is reportedly raising $4 billion in a new funding round.

A collection of app developers and consumer groups want Europe to enforce laws against Apple.

-

Fintech6 months ago

Fintech6 months agoRace to Instant Onboarding Accelerates as FDIC OKs Pre‑filled Forms | PYMNTS.com

-

Cyber Security7 months ago

Cyber Security7 months agoHackers Use GitHub Repositories to Host Amadey Malware and Data Stealers, Bypassing Filters

-

Fintech6 months ago

DAT to Acquire Convoy Platform to Expand Freight-Matching Network’s Capabilities | PYMNTS.com

-

Fintech5 months ago

Fintech5 months agoID.me Raises $340 Million to Expand Digital Identity Solutions | PYMNTS.com

-

Artificial Intelligence7 months ago

Artificial Intelligence7 months agoNothing Phone 3 review: flagship-ish

-

Fintech4 months ago

Fintech4 months agoTracking the Convergence of Payments and Digital Identity | PYMNTS.com

-

Artificial Intelligence7 months ago

Artificial Intelligence7 months agoThe best Android phones

-

Fintech7 months ago

Fintech7 months agoIntuit Adds Agentic AI to Its Enterprise Suite | PYMNTS.com