This has contributed to CashPro netting more than 40,000 corporate and commercial clients around the world. The global treasury management platform now supports everything from mobile-based biometric logins to self-service forecasting using machine learning. “Clients … are looking for more productivity and efficiency out of tools that help them manage cash, payments and receivables,” said Tom Durkin, global product head of CashPro in Global Payments Solutions at Bank of America. According to Durkin, the cash flow managed by BofA’s corporate clients sits on top of a treasure trove of data for all the different systems that run through the bank. Globally, he told PYMNTS, exchanging information from trade, supply chains and foreign exchange provides unique visibility into a company’s treasury operations.

Durkin said CashPro now delivers “predictive, more personalized recommendations to clients to help drive the right treasury decisions [via a secure platform],” citing CashPro Forecasting, CashPro Chat and QR Sign-In as examples.

The Internal Stack

Bank of America has embedded AI not only in its client-facing products but throughout its internal technology stack.

“We’re leveraging AI … to help [develop] software,” said Andrew McKibben, head of International Technology and CIO for Global Corporate and Investment Banking at BofA. “It improves the productivity of a software engineer — helps them write code, helps them write test cases [and] improve time to market. It improves quality as well.”

McKibben said that innovation is decentralized by design. “We [believe] that all employees can innovate or be forward-thinking, regardless of their role,” he said. “We showcase it and we celebrate it.”

That approach has yielded more than 7,800 patents from nearly 8,000 employees, with 1,400 of those patents in AI and machine learning.

The bank’s “Great Wall of Patents” in the Chicago office, with members of the CashPro team. From left: Adam Jalali, Trish Gillis (patent holder), Scott Mumma (patent holder) and Alyssa Salloum. Credit: Bank of America

In generative AI, the bank’s efforts include content classification, summarization, and generation, which enables Bank of America to support clients more efficiently and effectively.

“You can prompt and ask questions of all of our research reports in a library and generate content that might be useful [for someone internally, or in discussions with] a client,” McKibben said.

Forecasting Efficiency

On the treasury side, Durkin pointed to CashPro Forecasting as one of the clearest examples of AI-driven efficiency. It learns from a client’s historical cash flows, automatically selecting the most accurate balance for each account and using it to forecast future cash positions. At the end of each day, the models are retrained based on the new cash flows from that day, allowing them to continuously learn and adjust for changes in seasonality and other operational impacts specific to each company.

“There’s nothing more important to the treasurer than preserving and understanding where their cash is,” Durkin said, adding that people traditionally have used a spreadsheet to forecast, and that could take up to a week to complete. By the time it’s done, the data is out of date. However, with CashPro Forecasting, the modeling is done within minutes.

CashPro Forecasting also supports scenario-based modeling. “If I create certain models and events, how will the model scenario work? How will that work within this unit — if I have a subsidiary operating in the EU versus a subsidiary that’s operating out of Brazil?” Durkin said. Clients can develop forecasts up to a year into the future.

In addition to forecasting, clients are increasingly using self-service features like account verification letters to do things like substantiate account information for a beneficiary. Bank of America said adoption has soared by 21% in the first quarter of 2025 from the fourth quarter of 2024.

Durkin said their clients no longer have to call the service center — they can generate the letters themselves. Clients are now asking the bank to offer the feature outside of the U.S. as well.

CashPro Chat is another artificial intelligence tool built on the same platform as Erica, the bank’s consumer-facing virtual assistant. CashPro Chat helps treasurers and other financial professionals to quickly view transactions, find information about their accounts and navigate CashPro functionality. According to Durkin, 40% of queries are self-serviced through this tool.

The evolution of the CashPro App is another core part of the bank’s strategy. “The app itself really started as … a transactional tool,” Durkin said. “But we see more opportunity for [it] to be a personalized tool [once] you’ve told it what you like, what you don’t like, and what you want to tap into.” A key demonstration of the app’s popularity is how it’s used to approve payments. Last year, the volume of payment approvals exceeded $1T. The bank believes the figure underscores the trust that treasurers have in the app to conduct strategic business decisions.

Saving Grace

Daylon Bailey, treasury operations manager at Highgate Hotels, said the CashPro App has been “our saving grace. Primary administrators like myself, a lot of times, we’re generally going into CashPro App to make decisions, so it’s nice to have front and center that information that we need right then and there — whether I need to approve a user change, I need to approve a wire or look at positive pay. It’s very intuitive. It’s like having the web-based platform in the palm of your hand.”

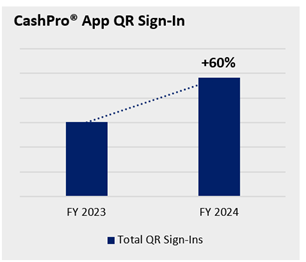

McKibben highlighted security as a key trend. The bank is adding additional security layers for protection, including stronger authentication through QR sign-in and push notifications before signing in. Push code notifications were added in May while adoption of QR sign-in is growing rapidly, increasing 60% from 2023 to 2024.

CashPro Insights is another capability that delivers value as it helps corporate clients make smarter treasury decisions by analyzing their transactional data. It provides tailored recommendations, such as encouraging shifts from paper checks to digital payments and highlighting opportunities to enhance account security. CashPro Insights is designed to “drive efficiency” and help clients better understand “what they should be doing, not just what they are doing today,” Durkin said.

Angela Brown, assistant treasurer of Continental, said, “the amount of data we can now tap into using CashPro Insights is jaw-dropping. We had been creating these KPIs internally and it took us many steps to get to these same valuable data points. Now they are right at our fingertips.”

Clients are responding to the improvements. “Some customers will say, ‘CashPro knows more about my business than some of my team does,’” Durkin said. “Because it sees all that.”

On the subject of agentic AI, McKibben said the bank is being deliberately strategic. “We’re interested in building that, but we also want to make sure we have the right controls around its use,” he said. “We’re deep into evaluating it.”

CashPro also offers flexibility, which is also a key differentiator.

“CashPro can meet the clients wherever they are, whether through the mobile app, online platform, or an API rail,” Durkin said. “Some clients may pull real-time data through the CashPro API, use the online experience for CashPro Chat, and rely on the mobile app to review and approve payments.”

Looking ahead, Durkin said more automation and intelligence are coming. “We’re going to continue to drive that out in areas where clients gain better access to information and more efficient delivery.”

McKibben said the broader trend is toward real-time treasury capabilities. “[Traditionally the data available to treasurers was based on what is already available but increasingly, data is becoming more ‘real-time’]. You want customers to get really valuable insights into the data and their cash flow to make more dynamic … decisions… That’s a continued focus area for us.”

Durkin closed with a reflection on CashPro’s future: “I think it’s already pretty smart, but as with any human, you’re never done learning.”

Cyber Security3 weeks ago

Cyber Security3 weeks ago

Cyber Security3 weeks ago

Cyber Security3 weeks ago

Fintech3 weeks ago

Fintech3 weeks ago

Artificial Intelligence3 weeks ago

Artificial Intelligence3 weeks ago

Fintech2 weeks ago

Fintech2 weeks ago

Latest Tech News3 weeks ago

Latest Tech News3 weeks ago

Latest Tech News3 weeks ago

Latest Tech News3 weeks ago

Fintech2 weeks ago

Fintech2 weeks ago